Foundations have long been associated with philanthropy and public good. However, they are often used as sophisticated tools by the super-rich to evade taxes and maximize profits. These mechanisms, while technically legal, exploit systemic loopholes, intertwining wealth preservation, influence, and control. Let’s explore how foundations and related strategies serve as vehicles for tax avoidance, profit generation, and power consolidation: foundations and tax evasion.

Tax evasion and avoidance strategies

The super-rich employ foundations as effective tax shelters. By donating significant assets to foundations, they gain large tax deductions. Often, these assets are stocks or appreciated properties. This strategy avoids capital gains taxes while reducing taxable income. Once donated, these assets grow tax-free within the foundation.

A prime example is the use of donor-advised funds (DAFs). These allow donors to claim immediate tax deductions while delaying actual charitable distributions. Although managed by an intermediary, the donor retains influence over the assets. Income-producing properties are also shifted to foundations. This reduces personal income taxes while allowing the assets to generate tax-free revenue for the foundation.

Foundations also exploit international systems. By donating to charities in tax havens, they take advantage of favorable tax laws. Offshore trusts often link to these foundations, further obscuring asset origins and minimizing taxes. These structures are particularly effective in evading scrutiny from local tax authorities.

Another common tactic is the revaluation of assets. Before transferring them to a foundation, their value is deliberately undervalued. This minimizes gift or estate taxes. Later, the assets’ values appreciate significantly within the tax-free shelter of the foundation. Similarly, deferred compensation plans allow executives to delay taxes on income or stock options by channeling them into foundations.

Profit maximization techniques

Beyond tax avoidance, foundations indirectly maximize profits. Self-dealing is a key strategy. Foundations often hire family members, purchase services from donor-owned companies, or invest in ventures linked to the donor’s business interests. While these practices technically comply with legal boundaries, they funnel profits back to the donor under the guise of charitable activity.

Investments in private companies are another avenue. Foundations frequently channel funds into private equity or venture capital. This yields high returns while allowing the foundation to act as a tax-free investment vehicle. The profits generated indirectly enrich the donors’ broader portfolio.

Strategic philanthropy is another tool. Donors align their giving with their business interests. For example, funding renewable energy research might support their private ventures in green technology. Similarly, donations to healthcare initiatives often benefit pharmaceutical companies owned by the donor. These calculated moves blur the line between altruism and profit-seeking.

Real estate plays a significant role. Foundations acquire large tracts of land under the pretext of conservation. However, these lands often increase the value of surrounding properties owned by the donor. In some cases, the land is later repurposed for commercial use, generating significant profits.

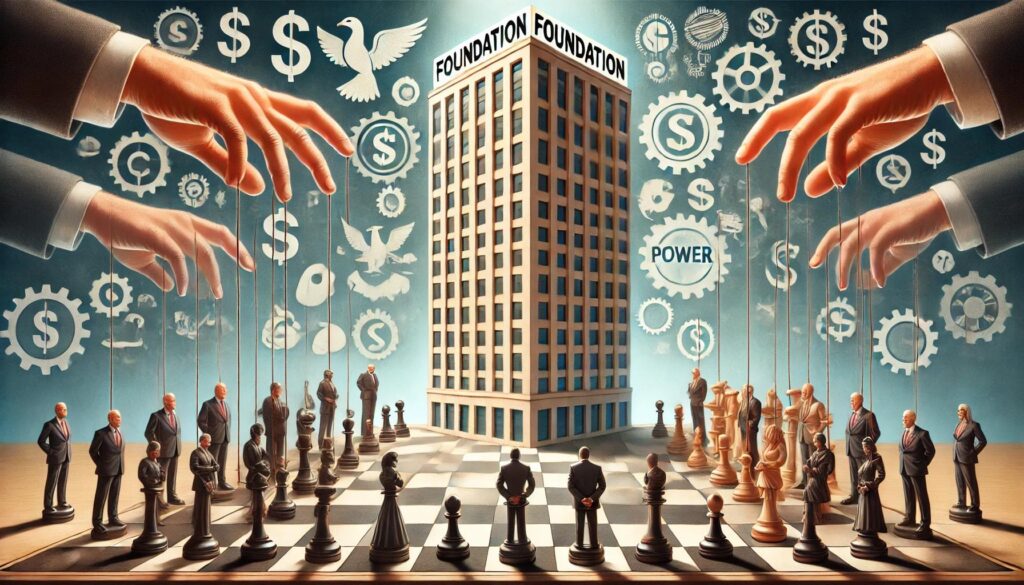

Influence through philanthropy

Foundations serve as powerful tools for shaping public policy, media narratives, and societal priorities. Through grants to think tanks, research institutions, and lobbying groups, they influence laws and regulations favorable to their interests. While direct lobbying is restricted, indirect funding channels achieve the same outcome.

Media influence is another area of concern. Foundations often fund journalism under the guise of promoting investigative reporting. In reality, this allows them to control narratives and protect their reputations. Academic funding operates similarly. Donations to universities often come with strings attached, ensuring that research aligns with the donor’s agenda. For instance, studies funded by oil companies’ foundations frequently downplay environmental concerns.

Not just foundations and tax evasion: International investments and political bribery

A less overt but equally troubling strategy involves investing in foreign countries while bribing local politicians. These practices allow the super-rich to establish influence not only in those countries but also indirectly in the United States. By controlling key industries or sectors abroad, they gain leverage over international markets and policies. This influence often translates into greater power at home, as they shape trade agreements, regulations, and geopolitical strategies to their advantage.

For example, individuals like Bill Gates have been accused of using philanthropic ventures to push personal agendas. Gates’ foundation often invests in foreign agricultural projects, ostensibly to combat hunger or improve sustainability. However, these initiatives sometimes promote genetically modified crops or technologies tied to companies in which the foundation has financial stakes. By aligning foreign aid with private interests, these individuals can dominate local economies and build networks of loyal politicians and business leaders.

Bribing local politicians ensures favorable policies, reduced regulations, and preferential treatment. These connections enable the super-rich to bypass restrictions and secure lucrative contracts. This method effectively creates a cycle of dependency, where foreign governments and industries are beholden to the donors’ interests. In turn, this global influence bolsters their standing in the United States, further insulating their wealth and power.

Wealth concealment and preservation

Foundations act as vehicles for generational wealth preservation. By operating in perpetuity, they keep wealth tax-protected indefinitely. Family members often serve on foundation boards, earning salaries while maintaining control over the assets. This creates a tax-exempt family office disguised as a philanthropic entity.

Art and cultural assets further illustrate this tactic. Donating valuable artworks or artifacts to museums controlled by foundations avoids inheritance taxes. These assets remain within the family’s influence while appreciating in value. Some foundations also lend these items to public institutions, gaining prestige while retaining ownership.

Program-related investments (PRIs) are another tool. Foundations use PRIs to fund for-profit ventures that align with their charitable missions. This creates a legal loophole, enabling tax-sheltered investments in private businesses. For example, a foundation might fund a healthcare startup under the guise of improving public health, even if the primary goal is profit.

Reputation management and soft power

Philanthropy provides a convenient cover for controversial business practices. Known as “reputational laundering,” donations to public causes mask unethical behavior in other areas. For instance, a billionaire profiting from fossil fuels might fund environmental initiatives to repair their public image.

Foundations also act as gatekeepers. By controlling which causes and communities receive funding, they disproportionately influence societal priorities. This consolidates their soft power, ensuring they remain central to public discourse and decision-making.

Legal loopholes and minimal oversight

The regulatory framework surrounding foundations is often weak. Current laws allow minimal oversight of how funds are used or invested. For example, U.S. law requires foundations to disburse only 5% of their endowments annually. The rest can grow tax-free indefinitely. Many foundations exploit this, spending just enough to maintain their tax-exempt status while retaining the majority of their wealth.

Opaque structures compound the problem. Layering foundations, trusts, and shell companies creates a labyrinth of financial vehicles. This makes it nearly impossible for tax authorities to trace wealth or enforce compliance. Some foundations even charge endowment management fees, funneling money back into firms owned by the donors.

Calls for reform

Critics argue that the current system enables the public to subsidize private wealth. Every tax-deductible donation reduces government revenue, shifting the tax burden to ordinary citizens. Proposals for reform include increasing mandatory payout rates, taxing unrealized gains within foundations, and imposing stricter oversight on program-related investments.

Conclusion

Foundations are not merely philanthropic tools. For the super-rich, they represent a sophisticated system for evading taxes, maximizing profits, and consolidating power. These practices, while legal, expose systemic flaws that allow a few individuals to dominate economic, social, and political landscapes. Without meaningful reform, foundations will continue to serve as vehicles for wealth preservation and influence, rather than genuine agents of public good.

Leave a Reply