They often say that Jewish backstabbing of Germany during WWI is a conspiracy par excellence. But since we know that some conspiracies are not actually conspiracies, what was the reality?

You can have every possible objection (as I do) to highly organized banking dynasties and super-rich families that are based on religious clientelism (regardless of the religion). However, it is true that members of those structures often do not marry outside their religion. But no, there wasn’t any anti-German sentiment within those power circles.

The reality is that Jewish highly organized clientelism did, in fact, finance the Allies more. However, the reasons had nothing to do with nationalism or anti-German sentiment. So, claiming otherwise would be flat-out anti-Semitism.

Jewish backstabbing Germany? Big money rules it all

Jewish bankers supported the Allied effort, particularly from American banks. All of because the highly organized Jewish clientelism has an unimaginable amount of assets in the US banks. There is an aspect that some American super-rich families are repulsed by them. This lasts to these days. Now you see the power they exert over the president or the power of the Israeli lobby.

These bankers, who held significant influence in the financial world, prioritized their international connections and provided crucial loans to Britain and France. This weakened Germany’s ability to finance its war effort.

These banks are interconnected through ownership stakes, shared board members, and secret agreements.

The financial support that the Allied Powers received from the United States, particularly from institutions like J.P. Morgan & Co., was driven by economic interests rather than any ethnic or religious loyalty. J.P. Morgan & Co. acted as the purchasing agent for the Allies in the U.S. and facilitated large loans. But this was no Jewish backstabbing because the Allied nations were seen as a better financial risk than Germany. Especially after the U.S. entered the war on the side of the Allies in 1917.

Geopolitical reasons

One of the major reasons why American banks, particularly those based in New York, gave more loans to the Allied powers than to Germany was simple economics. The Allied nations, including Britain, France, and Russia, had far more substantial trade ties with the United States than Germany did. Britain, for example, was a vital trade partner, and American businesses and banks had significant financial interests tied to the British economy. When Britain imposed a naval blockade on Germany, cutting off its access to international trade, American firms found it much harder to conduct business with Germany. The blockade strangled Germany’s economy and made it less attractive for American banks to provide loans, as repayment seemed increasingly uncertain. So no Jewish backstabbing.

WW1: Banks betting on the winner

Furthermore, the security of loans played a crucial role in these decisions. By 1917, it was becoming clear that Germany was struggling both militarily and economically. The long war had drained its resources, and with the blockade firmly in place, its economy was suffering. In contrast, the Allies, despite their own hardships, had vast global resources at their disposal, including colonies, which made them seem like a safer investment. American banks, which operate based on profit and security, saw the Allies as more creditworthy. Loans to Britain and France were thus considered less risky. Because these nations were more likely to repay debts due to their stronger economic and colonial positions.

This dynamic intensified after the United States entered the war in 1917 on the side of the Allies. With the U.S. government now fully committed to the Allied cause, American banks became even more involved in financing the war effort. Prominent financial institutions, such as J.P. Morgan, became official agents for British and French loans, ensuring a continued flow of American money into the Allied war chest. The U.S. government encouraged this support as it aligned with its own strategic and military goals.

Jewish backstabbing: So who was the alleged Jewish puppet master?

The antisemitic conspiracy theory that blamed Jewish financiers for Germany’s financial isolation (Jewish backstabbing) was fueled by stereotypes and racist narratives rather than actual financial or political realities. Jewish bankers in the United States, such as those associated with the firm Kuhn, Loeb & Co., did play a role in international finance. But they guided their decisions by the same economic logic as any other banker’s – based on creditworthiness and profit, not religious or ethnic allegiance.

For example, they often accused Jacob Schiff, a prominent Jewish-American banker, of deliberately undermining Germany which they saw as Jewish backstabbing. But this claim ignores the broader economic context in which Schiff and others operated.

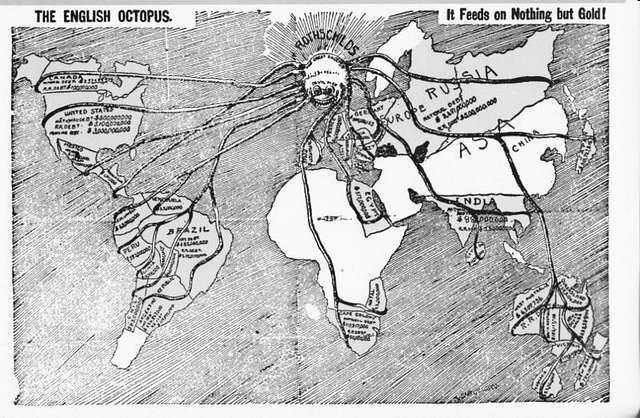

The Rothschild family, another frequent target, had banking branches across Europe, including in both Britain and Germany.

However, the idea that they – or any Jewish financiers – united to orchestrate Germany’s defeat is entirely unfounded. The Rothschilds, like other bankers of the time, were divided by national interests. And their business decisions were made according to the economic pressures of the day, not by any coordinated effort to harm Germany.

Crazy conspiracy, then reality check!

Ultimately, the theory that Jewish bankers “betrayed” Germany is part of the broader Dolchstoßlegende. This sought to explain Germany’s defeat by blaming internal enemies, including Jews, socialists, and communists. In the chaos of post-war Germany, far-right nationalists latched onto this myth to deflect blame from the military and political leadership that had actually led the country into disaster.

The “stab-in-the-back” myth (Jewish backstabbing) became a convenient and dangerous narrative the Nazi regime used to justify their policies of persecution and genocide.

People fueled this theory by the social and economic upheaval in Germany following the war, including hyperinflation, political instability, and the harsh terms of the Treaty of Versailles.

These conditions created fertile ground for scapegoating. And they falsely accused Jews of various forms of betrayal, including financial treachery.

The reality was far more complex and grounded in the financial interests of the time. U.S. banks loaned more to the Allies because they saw them as more likely to win and repay their debts. Not because of any conspiracy. The antisemitic lens through which these financial decisions were later viewed helped fuel the dangerous rise of radical nationalism in Germany, with tragic consequences.

Where was the greatest anti-semitism before WW1? France or Germany?

Anti-Semitism in France before World War I was more publicly visible and politically divisive due to the Dreyfus Affair. The case not only exposed deep-rooted anti-Jewish sentiment. But also became a national crisis, drawing in intellectuals, political parties, and the media in a battle over justice and national identity. The affair polarized French society, with anti-Semitic factions gaining traction, especially among conservatives and Catholic groups, while progressive and left-wing movements fought for Dreyfus’s exoneration. The visibility of this scandal made anti-Semitism in France highly charged, deeply affecting the country’s political landscape.

In contrast, Germany’s anti-Semitism, though pervasive, lacked a single explosive event like the Dreyfus Affair. Anti-Jewish sentiments were widespread in nationalist and conservative circles, and political parties openly espoused anti-Semitic rhetoric. However, the issue remained more of an underlying societal and political force rather than a national crisis. While anti-Semitism in Germany was steadily growing and would later culminate in more extreme forms, it did not dominate public debate as it did in France during this period. Therefore, in the years before WWI, France’s anti-Semitism was more publicly intense. Even though both countries are steeped in prejudice.

Of course, the Rothschilds had assets both in Allied countries and Germany. But what would be the reason for betraying Germany? Less antisemitism? No. Only economic reasons prevailed. So no Jewish backstabbing.

Banks no longer lend money to war efforts

After World War II, the global community faced the urgent need to prevent the conditions that had fueled two devastating global conflicts within a span of just a few decades. Among the many lessons learned, one was the role that financial institutions had played in funding the war efforts of nations, often without regard to the consequences. Banks and financial systems had enabled the production of arms, funded military operations, and, in some cases, directly profited from the destruction and chaos that wars brought. This led to a growing realization that financial systems needed to be reformed to prevent such support for conflicts in the future.

The post-war period saw the establishment of the Bretton Woods Agreement in 1944, which aimed to create a stable global financial system. Although its primary focus was on economic recovery and international stability, the agreement indirectly supported efforts to prevent war financing by creating institutions like the International Monetary Fund (IMF) and the World Bank. These institutions were designed to promote economic cooperation, reconstruction, and development, particularly in war-torn regions, with the understanding that economic stability could act as a bulwark against future conflicts. By channeling financial resources into rebuilding and development rather than militarization, the post-war world sought to create a foundation for lasting peace.

The Geneva Conventions

In the years following the war, international regulations began to address the role of banks in financing conflicts more directly. The Geneva Conventions of 1949, while primarily focused on the humanitarian treatment of civilians and prisoners of war. It had also implicitly raised concerns about the resources that fuel wars, including financial ones. The growing influence of the United Nations further contributed to the idea that financial institutions should remain neutral in conflicts. The UN’s peacekeeping efforts and the use of sanctions, including financial ones, aimed to curb the ability of aggressor states to fund wars. In particular, the UN imposed financial restrictions on countries that violated international norms. This was signaling a shift toward limiting the flow of money that could be used for war efforts.

Ethical banking

At the same time, the post-war era saw the emergence of ethical banking and socially responsible investing. This emphasized the importance of financial institutions considering the broader social and political impacts of their actions. This movement, which gained traction in the latter half of the 20th century, argued that banks and investors should avoid financing industries that contributed to war, such as arms manufacturers or companies operating in conflict zones. The concept of “ethical banking” was bolstered by public outcry against the profits made by some banks during World War II, particularly Swiss banks. These banks found to have held assets seized by the Nazis. This scandal reinforced the need for financial institutions to adopt more responsible practices.

Many large financial institutions began implementing internal policies that restricted their involvement in industries connected to war. Some banks introduced guidelines to avoid lending to companies involved in arms production or military-related industries. This shift was partly driven by public pressure and partly by the recognition that a bank’s reputation could be harmed if it was seen as complicit in fueling conflicts. Additionally, the rise of socially responsible investment (SRI) practices led to investors increasingly factoring in environmental, social, and governance (ESG) considerations, including a company’s involvement in war-related activities.

Freezing assets

As global conflicts persisted into the 21st century, financial regulations related to war financing became even stricter. Particularly with the introduction of anti-money laundering (AML) and counter-terrorism financing (CTF) laws. These regulations, which gained momentum after the September 11, 2001, attacks, aimed to prevent the flow of funds to terrorist organizations and states engaged in illegal warfare. They required financial institutions to monitor and report suspicious transactions, freeze the assets of individuals or groups connected to terrorism or conflict, and avoid doing business with regimes involved in serious human rights violations or aggressive military actions. These laws placed banks on the front line of efforts to disrupt the financial networks that could sustain prolonged conflicts.

International weapon trade

Furthermore, the international community continued to push for greater regulation of the arms trade and its financing. The adoption of the Arms Trade Treaty (ATT) in 2013 marked a significant step in regulating the international trade of conventional weapons. The aim was to reduce the flow of arms into conflict zones. Although the treaty primarily targeted arms dealers and manufacturers, it also underscored the need for financial institutions to ensure that they were not financing arms deals that could contribute to war. This created additional pressure on banks to exercise caution when providing financial services with possible links to military-industrial complex.

In conclusion, the post-World War II resolution to prevent banks from financing war efforts was not the result of a single decision but rather a series of developments in international law, financial regulations, and ethical investment practices. While institutions like the IMF and World Bank were created to promote peace and stability through economic cooperation, subsequent efforts targeted the specific role of financial institutions in conflict. The rise of responsible banking, stricter regulations on arms financing, and the implementation of AML and CTF laws have all contributed to reducing the likelihood that banks will fund wars. The global financial system, once a tool that facilitated conflict, is now increasingly seen as a key player in the effort to prevent it.

Creating global dominance and why war financing can be detrimental to their interests

The restriction on war financing by banks is part of a broader agenda by the global elite. A small group of powerful individuals or organizations, including major international banks, governments, and global institutions like the IMF or the World Bank, are working to centralize control over the global financial system (and successfully).

This prevents banks from funding wars. These elites can manipulate global power dynamics, creating dependence on certain financial structures and restricting nations from independently waging wars.

Also, banks found that is better not to fight, gaining their wealth by other means. This also means greater cohesion in the West, even though respective power structures have their feuds.

Conclusion

In summary, the conspiracy theory that Jews “backstabbed” Germany during World War I by allegedly providing loans to the Allies is completely unfounded and rooted in antisemitic propaganda. It distorts historical realities and was used as a tool by the Nazis to fuel hatred and justify their persecution of Jews. The financial dealings during the war were driven by economic considerations, not by any ethnic or religious conspiracy.

Banks, fortunately, don’t lend money to war efforts now, therefore there was peace for a long time.

Leave a Reply